We're building something new – take a look at the beta site: intglobal.com

A number of banks around us are working hard to innovate and create a unique customer experience using the possibilities of digital banking. However, the whole banking architecture needs to adapt to the required viability and flexibility to become future proof. A way to do it is to open up the bank’s capabilities to essentially empower anyone who wants to develop their own financial products and services- ‘Banking-as-a-Service’ (BaaS). Though this goes against the fabric of traditional banking as they had always preferred an end-to-end service delivery model. However, the recent consumer centricity that is taking over the market with born-digital FinTechs is big.

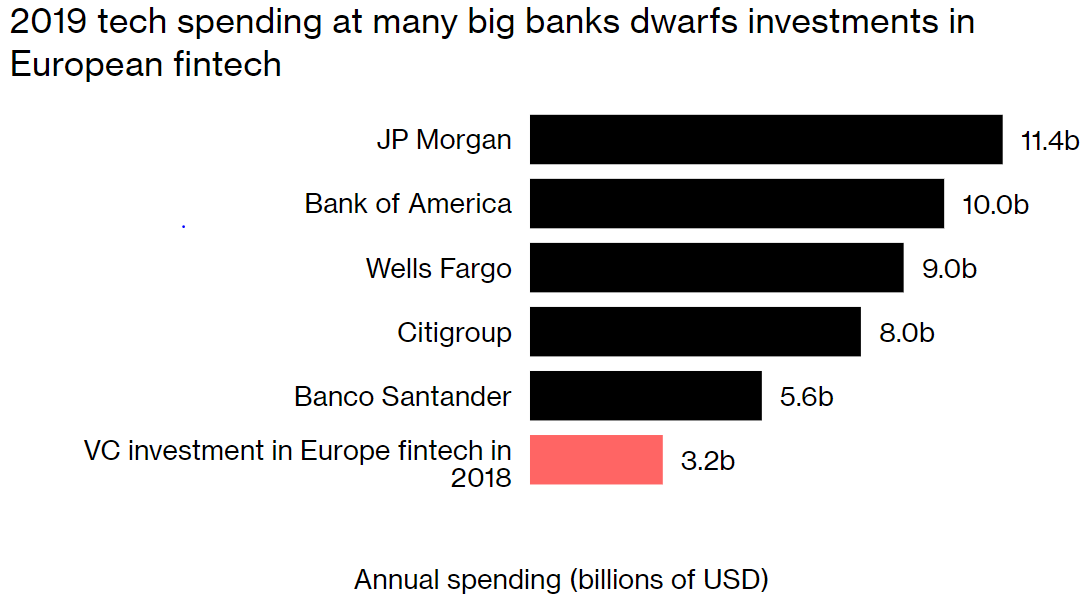

According to Bloomberg, most big banks are spending more on digital than the total investment in all the FinTech start-ups

Source: Bank disclosures, data compiled by Bloomberg and KPMG Pulse of Fintech Report based on Pitchbook data.

This data does give an idea as to where banks are heading to but don’t give us the complete picture. A number of instances like

All this collaboration shows how banking is gradually becoming a service and banking is not limited to the banks only. Another area of interest is open banking. So, what is the difference between BaaS and Open Banking?

Though BaaS goes hand in hand with Open Banking, however it relies on the collaboration of financial institutions, service providers and customers based on APIs. On the other hand, BaaS focuses on using APIs to provide simple access to banking and payment products while meeting regulatory requirements. These platforms help reduce the need for businesses to invest in their own technology and screening mechanisms as these platforms carry out all the processes needed for financial and regulatory operations.

Thus with BaaS a bank can use a module, component or function of a bank and allow FinTechs to create an application packaged and network-enabled as a banking widget. The balance statement widget; the payments transaction widget; the loan application widget; and so on.

For example, a personal finance company of Mint aggregates data from customer’s different accounts and provide bank-like service outside a bank-owned channel that is leveraged by open banking. While a company like Digit relies on access bank’s infrastructure to provide a host of services like automatic savings, overdraft prevention services that the bank doesn’t offer to consumers.

So how does BaaS work?

Some more examples;

Evidently, as BaaS emerges as a new business model and an effective competitive toolkit, banks must shift focus to financial management solutions assemblers.

An efficient BaaS implementation strategy should focus strongly on enabling plug-and-play operations which different Fintechs can plug and provide tailor-made services to meet customer needs. By adopting these methodologies, banks will also experience better standardization and cost reduction.

Starling bank’s Banking-as-a-Service partnership is with Raisin UK, the online savings marketplace that allows customers to pick the best savings deal on the market to meet their individual needs. The relationship allows Raisin UK to use Starling’s APIs to open accounts for each customer, collect their deposits and place them at their expanding network of partner banks that participate in its marketplace.

It is clear that there are a number of benefits in BaaS and in creating an API ecosystem. Banks will also find new revenue sources and acquire new customers, especially digital natives seeking more innovative offerings.

From a customer’s point of view, a BaaS platform enables them to take out loans at a digital point of sale, invest in funds at the push of buttons and also transfer money. Companies are able to combine payment functions directly with the rendering of services, for example supplying electricity, machine activities or transports.

In the current platform debates, we are led to believe that an API already makes a bank a platform – however it is merely a necessary technical requirement, but not a platform sufficient feature. They provide for varied features, for example, in Germany, the Wirecard Bank, Solaris Bank and the Sutor Bank operate BaaS platforms; each with different points of focus.