In the last five years, we have seen four times growth in the number of neobanks globally. In contrast with the reports, it is observed that from 2018 to 2020, there has been a dip in customer trust by 2.9%. So, Digital banking startups are in a tough spot.

Suppose we are thinking about the reason for the rise of neobanks (in numbers). In that case, it is because of their relentless approach towards customer-centricity, wooing them with an innovative tech stack and conveniently reaching out by means of modernised services. Then why are they losing customer’s trust?

According to the AT Kearny report, by 2023, neobanks are projected to have up to 85 million customers alone in Europe. A large customer base doesn’t mean neobanks have huge trust. An inverse relationship has been noted- a large customer base leads to a huge loss of profit for the neobanks.

Challenges led to the loss of trust.

Customer acquisition is expensive. New customers aren’t always profitable when there is less direct deposit relationship and huge compliance and customer service cost. Neobanks tends to overlook the lifetime value of a customer.

The pressure to attract new customers at a higher rate than their competitors has forced neobanks to provide high savings rates, low lending rates and discard many preliminary charges that lead to renouncing profits.

Later on, after increasing the customer base, these neobanks tend to change their pricing model and thus lose the trust of a highly engaged customer base.

Currently, the world is going through digital transformation, and everything around us is customer-focussed. Neobanks, to be the disruptor, need to act fast. Focussing on customer acquisition can provide short-term success, but neobanks need to develop a unique proposition for long sustainable growth. Today, “one-size-fits-all” is an old concept and neobanks need to become niche in its offer through a “customer-first bank”.

2-Key success factors for Neobanks

With rapidly changing customer behaviour and crowded market, neobank needs to provide unique offerings to stand out. Here is the list of top two ways where neobanks should narrow down the focus:

Meet the unmet needs for micro-savings and micro-insurance

In the neobanks sector, there are ample products in the market that fulfil the demand for stable incomes, but the uncertain income group segments find fewer products viable for them. Thus, neobanks may find a niche in providing financial services to the huge unbanked segment.

A goal-oriented approach to attract customers faster

A vast number of customers lack financial knowledge; thus, directly reaching out to them with the product will be a flawed strategy. Neobanks should come up with a more goal-oriented focus to attract customers faster than their rivals. For eg: a different sort of financial advice should be given to the person who wants to save for their children’s higher education and different for someone looking for starting a business. Shift from product-focused to goal-focused.

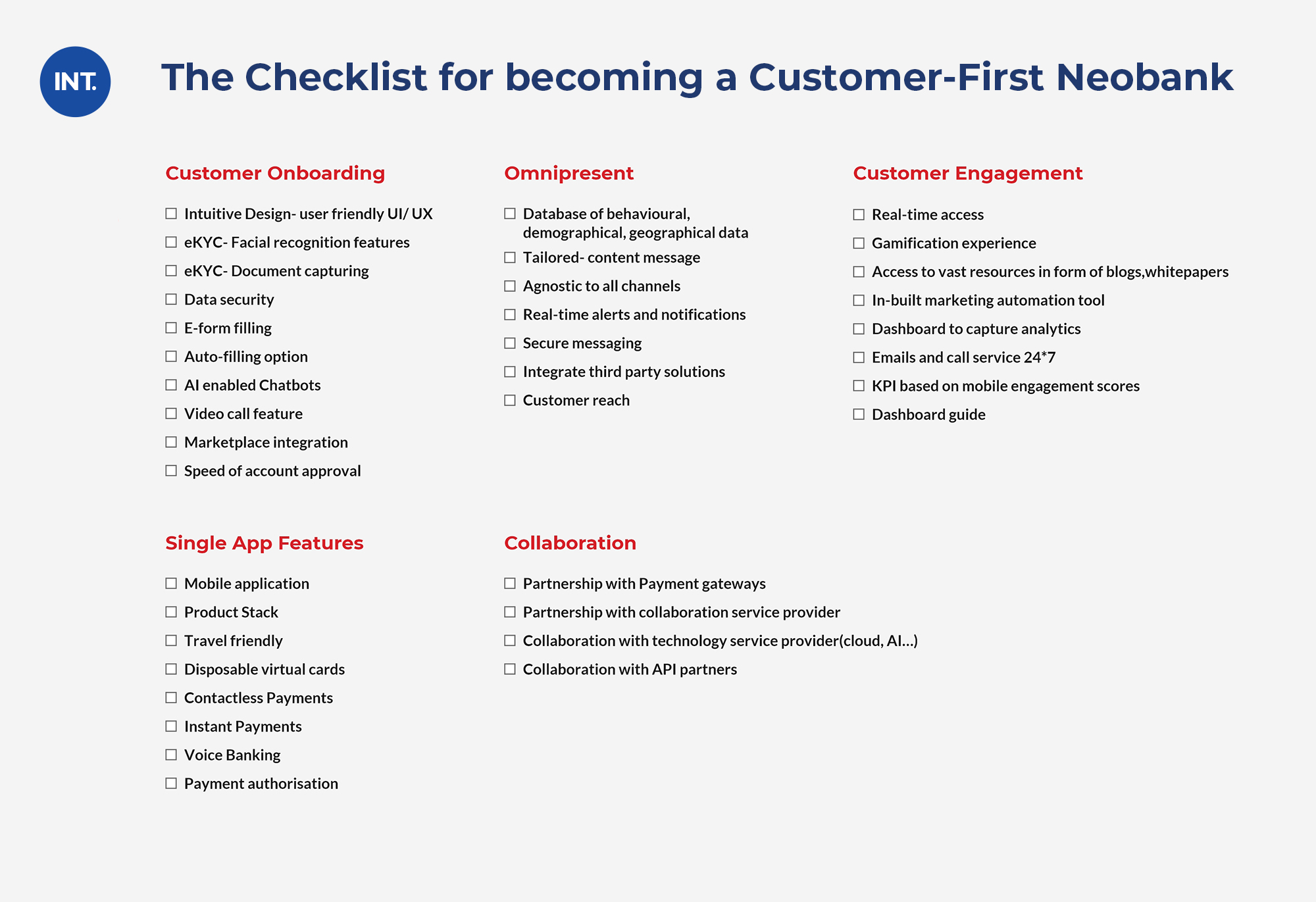

A tool kit for neobanks to become “Customer-First.”

We have been studying the neobanks market for a long and have realised that neobanks need to be customer-centric to disrupt the banking landscape by offering hyper-personalised products. Here is the checklist crafted after identifying the challenges neobanks are facing in 2021.

We know whether neobanks cater to the smaller segment or more extensive customer base, it becomes essential to build customer-centric systems and processes. Leveraging a strong voice led system for advising or high AI and computer visioned tech to enhance the front-end technologies, neobanks must adopt technology to provide financial services to the unbanked.